FROM STARTUP TO IPO: UNLOCKING A $100B+ OPPORTUNITY IN MENA

INTRODUCTION

MENA is one of the most attractive markets for the development of technology ventures – it has now reached an upward tipping point in its growth trajectory. We believe the region can output 45 unicorns by 2030, and can create digital giants that can list on public markets, remain independent, and keep their focus on delivering innovative solutions tailored to local needs. In this paper, we share some of our analysis and learnings and we take the opportunity to contribute our viewpoint on how to further enable and nurture the ecosystem with the participation of all players. We also share a playbook on scaling technology companies across multiple sectors and countries in the MENA region.

A SPIKE IN TECH DEMAND AND CRITICAL GAPS IN OFFLINE OFFERINGS CREATE LEAPFROG OPPORTUNITIES IN MENA

More than 55% of MENA’s population is younger than 30 years old and it is growing at a 1.6% per year rate. MENA’s population are avid consumers of digital media, with an average daily social media consumption of 3.5 hours. These statistics set MENA apart in comparison to any other region across the world.

MENA’s young, fast-growing, and tech savvy population has high spending power and is keen to utilize technology for shopping, transacting, learning, and socializing. This translates to a strong demand for digital products and services across industries. Technology ventures that have the ability to cater to the tastes of this attractive user base can achieve accelerated growth and deliver strong unit economics.

On the supply side, traditional offline offerings show significant gaps across different sectors, providing technology ventures with easy access to underserved users and consumers. Those gaps are especially apparent in the banking sector, where more than 45% of MENA population is still unbanked; and in the retail sector, where the leasable retail area per capita is still one fourth that of developed markets. Such gaps boost the Fintech and eCommerce opportunity and consequently lead to prolific venture activity.

The list of underdeveloped sectors offering leapfrog opportunities is long and includes logistics, which is still underdeveloped and extremely fragmented, as well as real estate discovery، purchasing, and financing, currently underserved due to lack of market transparency and the dominance of informal and non-professionalized network of independent real estate brokers.

THE EVOLUTION OF MENA'S TECH ECOSYSTEM IS AT AN UPWARD TIPPING POINT WITH AMPLE HEADROOM FOR GROWTH

In 2019, we projected in our ‘How Much Can the Venture Capital Industry Grow in Saudi Arabia by 2025?’ report that it would have taken 6 years for MENA and Saudi Arabia’s VC deployment to reach $2.6B and $500M, respectively. In reality, that was achieved in 2 years.

The growth of the technology ecosystem follows a power law rather than linear progression. This trajectory is characterized by a sudden acceleration that marks an upward tipping point. MENA witnessed this tipping point in 2021, with a steep increase of VC deployed capital and of growth-stage deals (defined as funding rounds larger than $5M). The acceleration of the economic and technological ecosystem is driven by a growing talent pool, tech infrastructure, consumer adoption, as well as broad macroeconomic and regulatory reforms. As these components reached critical mass, the ecosystem enjoys an exponential growth.

However, the ratio of VC development to GDP in MENA is still much lower than that registered by other countries and regions, showing that VC yearly invested capital still has room to grow at least 5-10X before catching up with peer regions.

MENA IS JUST GETTING STARTED IN UNICORN PRODUCTION WITH THE POTENTIAL TO OUTPUT 45+ UNICORNS IN THE NEXT 7 YEARS, WORTH $100B+ IN EQUITY VALUE

We analyzed the number of unicorns[2] produced over time in markets with GDP and/or population comparable to MENA such as Brazil, Germany, UK, India, and South Korea. We also included USA in the peer group after resizing its number of unicorns based on the GDP2 delta with MENA. We learned that the unicorn production trajectory follows an exponential path rather than a linear one. This trajectory is quite comparable across the analyzed markets.

Assuming MENA will follow a similar trajectory, we estimate it will produce 45 unicorns by 2030, 10 years after Careem became the first MENA unicorn. This top-down estimate is validated by our direct observation of a number of tech companies that year after year are approaching the $1B valuation mark. We believe that the STV Fund I portfolio has the potential to deliver a number of unicorns in the next 3-5 years.

At the same time, based on benchmarks of comparable markets, we estimate that the total equity value of the 45 predicted unicorns could reach $100B+, as some of those technology companies will reach a valuation much higher than $1B. In particular we believe that within the next seven years MENA will see the emergence of decacorns, a technology company worth at least $10B in equity value.

THE OPPORTUNITY FOR TECH GIANTS TO EMERGE IS STILL OUTSTANDING

Most regions globally have seen the emergence of a technology giant, a multi-sector and multi-country player that secured a massive customer base and sustainable competitive advantage.

A NUMBER OF DRIVERS SUPPORT THE EMERGENCE OF A REGIONAL TECH GIANT

There are several drivers that make the emergence of a tech giant a natural evolution of any regional ecosystem. Tech giants have a business model that provides them with a number of unfair advantages that translates to a semi-monopolistic power.

Network Effects: Some tech platforms benefit greatly from network effects, where the more users are on-boarded, the more valuable the service becomes. This flywheel is especially utilized by cross-country and cross-industry tech giants in an interconnected region, where network effects of one offering benefit the remainder.

Customer Retention: Digital giants typically offer a subscription option that provides valuable benefits to its customers such as free delivery or reward programs. These marketing tools have been proven to significantly increase customer retention and ARPU (average revenue per user).

Cross Selling: Once a player has secured a large customer base through its initial offering, it becomes cost efficient for them to cross-sell additional products and services. In other words, these players enjoy a lower CAC (customer acquisition cost) compared to single-offer players. The cross-selling power become particularly strong in players that have high-frequent interactions with their customers (eg. ride hailing, food delivery, eGrocery). The daily or weekly touchpoints with the customers favor a higher level of trust and awareness, and more frequent opportunities to cross sell a wide offering.

Customization: The collection of a larger data set, enables digital giants to extract superior insights to continuously fine tune its offering, pricing, and delivery to each customer.

Economy of Scale: Like in any other business, large scale unlocks not just cost efficiency but the opportunity to attract superior talents and increase R&D investments.

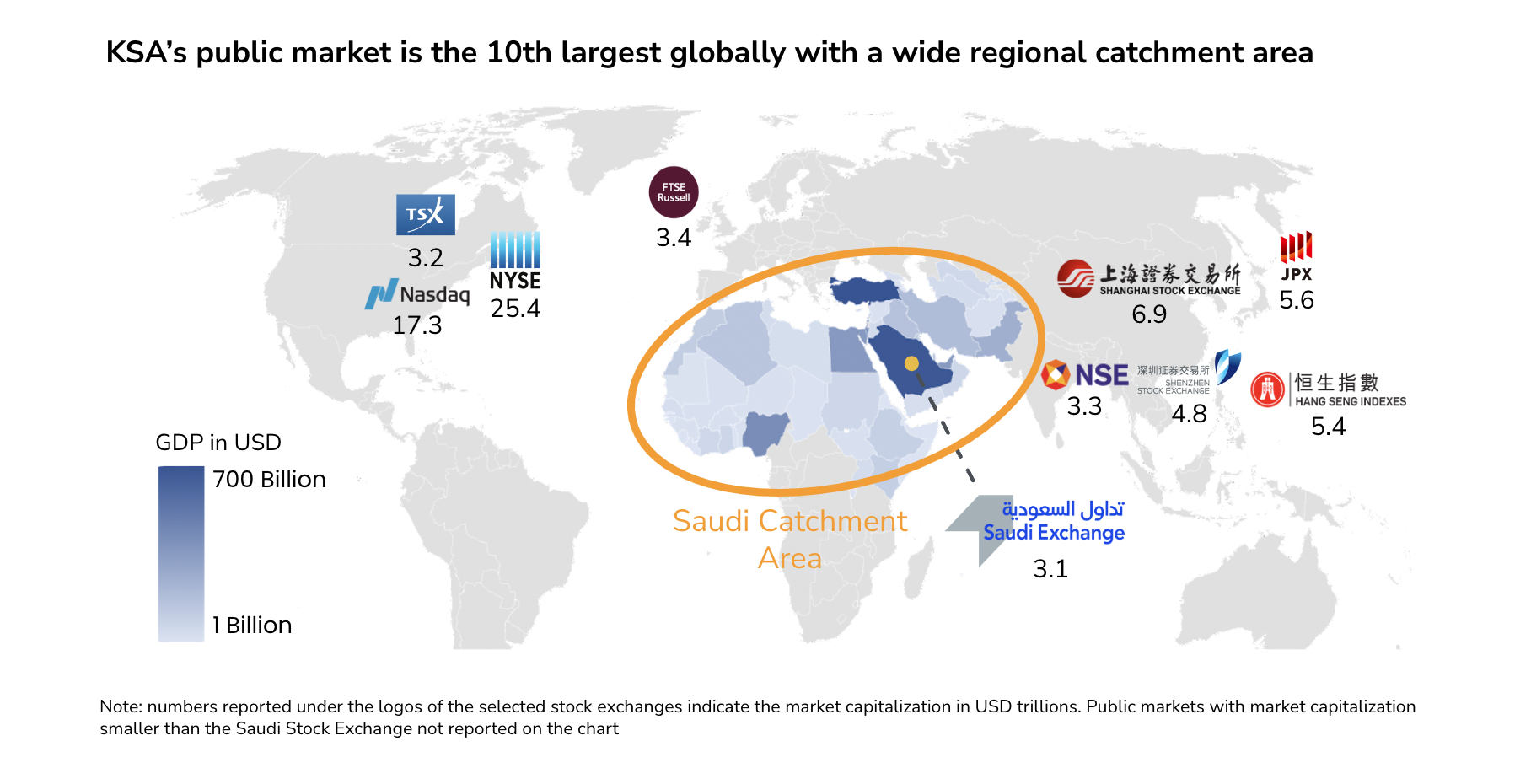

TWO EDGES MAKE SAUDI ARABIA THE NATURAL HOMEBASE FOR MENA DECACORNS: HIGH GDP & DEEP PUBLIC MARKET

With respect to scaling technology companies, Saudi Arabia is undoubtedly the gravitational center of the broader MENA catchment area, which also includes Central Africa, Southeast Europe, and Southwest Asia.

Saudi Arabia’s power of attraction is determined by two main drivers:

GDP size, which accounts for around one third of MENA’s total GDP. Cracking the Saudi Arabian market is necessary for most MENA startups that want to achieve unicorn status, irrespective of their initial country of origin.

Stock exchange size and depth, which is increasingly considered by VC investors as the preferred exit gate. Furthermore, the opportunity to exit through IPO positively impacts the strategy and the level of ambition of MENA tech ventures that are moving from developing a specialized and conventional offering to become attractive acquisition targets for global players, to developing solutions tailored more to the regional market with the vision to become self-sustainable regional leaders.

SAUDI ARABIA STOCK EXCHANGE DISPLAYS STRONG FUNDAMENTALS AND POSITIVE TRENDS

Saudi Arabia is going through a transformational phase, driven by the introduction of a multitude of programs and initiatives, the adoption of progressive regulations, and the support to nurture a vibrant private sector and growing talent pools. The KSA public market has recently seen positive reform that aligns with global best practices, leading to the inclusion of the Saudi public market in the MSCI and FTSE indices since 2019, as well as the first successful IPO of a VC-backed Saudi tech venture. This single IPO saw an oversubscription of 20X, showing a strong investor appetite for tech companies.

The role of regulators and government stakeholders has been pivotal in igniting this journey and attracting regional and international resources toward a clear and compelling vision, including:

The Financial Sector Development Program (FSDP), key in realizing Vision 2030, achieved major reforms in KSA public markets, evidenced by the inclusion of the Saudi market in international indices and the launch of derivative products. The program also resulted in the licensing of 3 digital banks, the launch of FinTech sandboxes under SAMA and CMA, the push for a cashless society, the launch of FinTech Strategy Implementation Plan, and the outlining of an open banking framework.

The New Saudi Companies Law, which tackles major legal obstacles for startups and VC investors through a flexible form of companies called “Simple Company” that allows for certain economic terms, minority control, and other customary VC terms not accepted under other company forms.

The opportunity provided by FinTech sandboxes that aim to test solutions before granting providers full licenses was critical to ignite this high-potential sector. The Open Banking policy outlined by SAMA in late 2021, which will require banks to adopt API policies, is a great first step towards digitization that will facilitate the emergence of innovative FinTech solutions as the ecosystem matures.

VC deployment in late-stage ventures creates market cap potential as a result of the high-growth and minority-interest style, multiplying the equity value of the initial investment. Our analysis indicates that the acceleration of late-stage investments creates a $100B+ market cap opportunity that can be captured in Tadawul by 2025. We are seeing early signs of realization, as Jahez IPO for example captured half of the the market cap potential in 2022.

As mentioned earlier, MENA presents a favorable context for the development of large technology companies. Today, the Information Technology sector’s share of the S&P500 is 48x larger than its counterpart on Tadawul. In only 5 years, technology companies took over the top ranking of US stock market. There is no reason why the technology sector on Tadawul cannot become as relevant as it is today in more developed markets.

To provide competitive IPO offerings and to enable an efficient and fast process for corporate action, corporate and tax requirements and policies need to align with the most competitive global markets. This will in turn reduce IPO waiting times and facilitate startup funding in a timely manner, as well as ensure that VC divestments meet fund lifetimes. These requirements include allowing governance and control for minority investors and minimizing dilution for founders, reducing the tax impact associated with corporate restructuring, minimizing capital gain tax in line with the most attractive jurisdictions, and standardizing treatment of resident and non-resident investors.

STV HAS IDENTIFIED A STRATEGY ON HOW TO DEPLOY CAPITAL AT SCALE TO CREATE AND ANCHOR DECACORNS IN SAUDI ARABIA

Working and strategizing side by side with our portfolio companies enabled us to identify a playbook for MENA ventures to scale up and to address two major challenges: the fragmentation of our region across a number of countries, and the often limited size of total addressable markets.

This playbook consists of three main phases: the first phase aims to grow the venture into a successful and sizable platform by cracking the Saudi market. The second phase focuses on cross-border expansion, and aims to inorganically boost the growth rate of the venture through M&A by leveraging the capabilities and know-how developed in phase 1. M&A represent an efficient tool to enter new geographies and product categories, and to overcome market size limitations of the initial focus. This is particularly applicable for markets with high barriers to entry and for companies whose products are challenging to organically scale across borders. Finally, phase 3 aims to maintain company independence – compared to being acquired by foreign entities – and to maximize growth potential through IPO.

There are a number of companies in our portfolio that are already in advanced stages of this playbook, and may soon have the opportunity to list publicly. We foresee several others that have the potential to follow a similar path as well.

MENA is on an unprecedented and accelerated path to unlock a $100B+ opportunity for tech ventures. This is driven by top-down reforms and initiatives, and is fueled by a young and tech savvy population, an integrated regional ecosystem, and a deep public market in KSA. We believe that the way to achieve this potential is through cracking the largest market in the region, replicating that success through in-organic growth channels, and finally maintaining regional independence while maximizing growth.

[1] Numbers for US, Canada, Singapore, Australia, KSA, and Oman are from multiple cities.

[2] Technology Companies that have reached an enterprise value higher than $1B

[3] US GDP ($22.7T) is 8.7X the GDP of MENA. In order to make USA comparable to MENA, in this chart we have scaled down the number of USA unicorns by a factor of 8.7.

[4] STV estimate based on comparative analysis of unicorn valuations in similar regions (Latin America, Europe, APAC)

[5] Listed market cap are as of market close on 31st of December of the listed year